The Qonto Smart Business Account Plan is designed for freelancers, sole traders, and small business owners who need advanced banking tools without the complexity of traditional business banking.

Positioned between Qonto’s entry-level and premium plans, the Smart plan provides enhanced payment capabilities, expense management tools, and accounting integrations to help businesses manage their finances efficiently.

Qonto has become a popular choice among European entrepreneurs thanks to its digital-first approach, transparent pricing, and business-focused features. The Smart plan is particularly attractive for growing businesses that require additional flexibility beyond basic banking services.

Explore how Qonto Smart can transform your financial management today.

Key Features of the Qonto Smart Business Account Plan

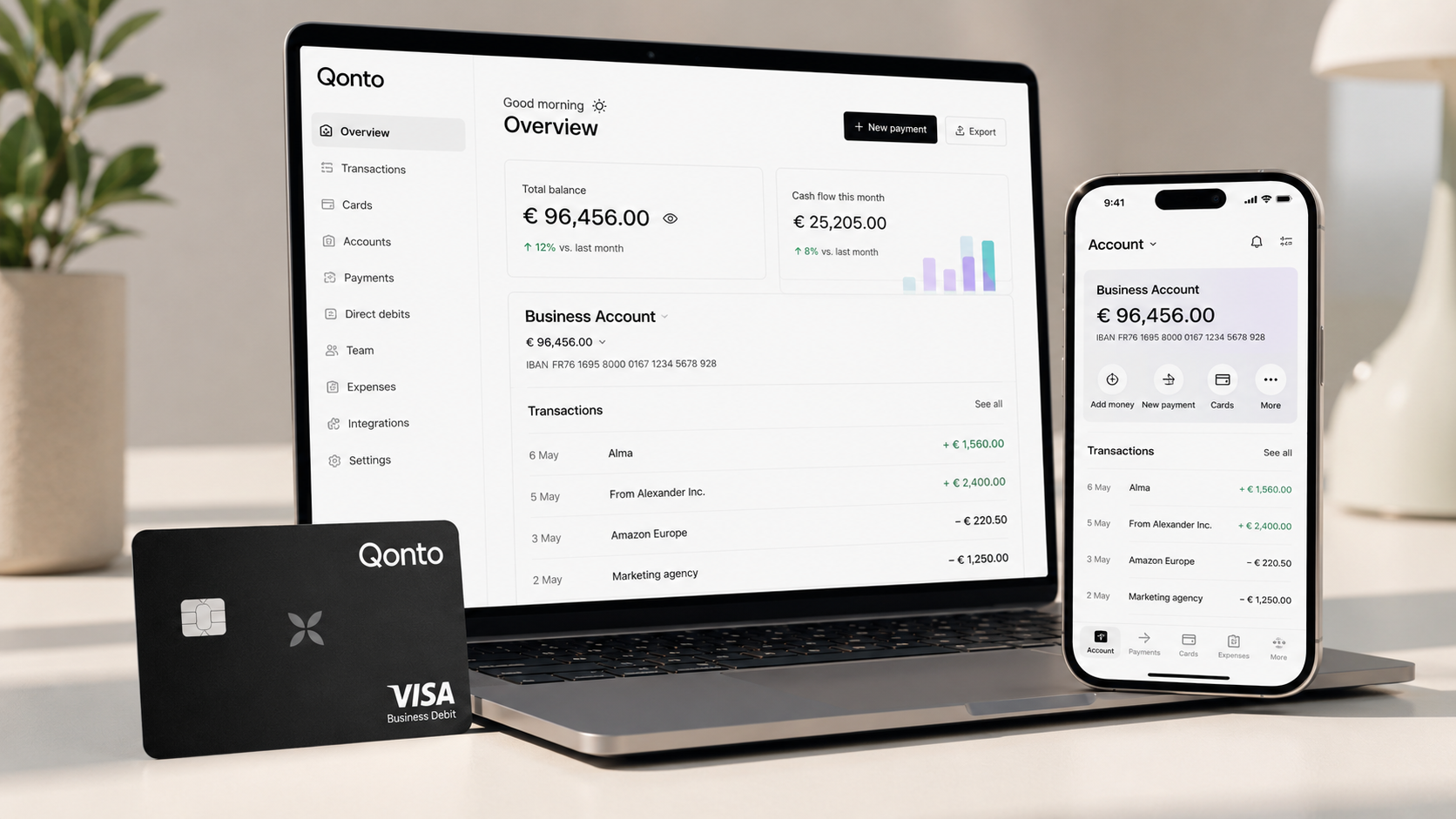

1. Dedicated Business IBAN

The Smart plan includes a dedicated business account with a local IBAN, enabling businesses to receive and send payments securely across Europe. This feature helps maintain a professional image while separating personal and business finances.

2. Physical and Virtual Mastercard

Users receive a Mastercard business card for everyday expenses. The Smart plan also supports virtual cards, allowing businesses to make secure online purchases while reducing fraud risks.

Key card benefits include:

- Online and in-store payments

- Contactless transactions

- ATM withdrawals

- Real-time payment notifications

- Card controls through the Qonto app

3. Increased Monthly Transaction Allowance

Compared to entry-level plans, the Smart Business Account offers a higher number of monthly transfers and direct debits. This makes it suitable for businesses with increasing transaction volumes.

Benefits include:

- SEPA transfers

- Direct debits

- Incoming payments

- Bulk payment capabilities

- Scheduled transfers

4. Expense Management Tools

One of the strongest advantages of the Qonto Smart plan is its built-in expense management functionality.

Features include:

- Receipt capture and storage

- Real-time expense tracking

- Expense categorization

- Team spending visibility

- Simplified bookkeeping

Business owners can upload receipts directly through the mobile app, helping reduce administrative work and improve financial organization.

5. Accounting Software Integrations

The Smart plan integrates with many popular accounting platforms, allowing businesses to automate bookkeeping tasks and reduce manual data entry.

Common integrations include:

- Xero

- QuickBooks

- Sage

- Pennylane

- Other accounting solutions depending on region

These integrations help accountants and business owners maintain accurate financial records while saving valuable time.

6. Multi-User Access

Businesses often require multiple team members to access financial information. Qonto allows companies to grant access to employees, accountants, and partners with customizable permissions.

This feature helps improve collaboration while maintaining security and control over company finances.

Qonto Smart Plan Pricing

The Qonto Smart Business Account Plan is typically positioned as a mid-tier option, offering a balance between affordability and functionality.

Pricing generally includes:

- Business account access

- Business Mastercard

- Monthly transfer allowance

- Expense management tools

- Accounting integrations

- Customer support

Since pricing may vary depending on country and promotional offers, businesses should verify the latest rates directly through Qonto before opening an account.

Benefits of Choosing the Qonto Smart Business Account

Streamlined Financial Management

Managing business finances becomes easier with centralized banking, payment processing, and expense tracking in one platform.

Time Savings

Automation tools reduce repetitive administrative tasks such as bookkeeping, receipt collection, and transaction reconciliation.

Improved Cash Flow Visibility

Real-time transaction monitoring helps business owners stay informed about incoming and outgoing payments.

Professional Banking Experience

A dedicated business account helps establish credibility with clients, suppliers, and partners.

Scalability

As a business grows, the Smart plan provides features that can support increased transaction volumes and larger teams.

Who Should Choose the Qonto Smart Plan?

The Qonto Smart Business Account Plan is ideal for:

Freelancers

Freelancers can manage invoices, payments, and expenses from a single platform while maintaining clear separation between personal and business finances.

Consultants

Consultants who handle multiple clients benefit from efficient expense tracking and seamless payment management.

Startups

Early-stage companies can take advantage of digital banking tools without the overhead associated with traditional banking institutions.

Small Businesses

Growing businesses gain access to additional transaction allowances, team access controls, and accounting integrations that simplify daily operations.

Discover how Qonto’s accounting integrations simplify your tax season today.

Qonto Smart Plan vs Basic Business Plans

Compared to entry-level business banking options, the Smart plan provides:

| Feature | Basic Plan | Smart Plan |

|---|---|---|

| Monthly Transfers | Limited | Higher Allowance |

| Expense Management | Basic | Advanced |

| Team Access | Limited | Enhanced |

| Accounting Integrations | Basic | Comprehensive |

| Business Tools | Standard | Expanded |

Businesses expecting growth often find that the Smart plan delivers greater long-term value due to its broader feature set.

Security and Compliance

Security remains a priority for modern business banking. Qonto incorporates multiple protection measures, including:

- Two-factor authentication

- Secure login protocols

- Card freezing and unfreezing

- Transaction monitoring

- Regulatory compliance standards

These features help protect business funds and sensitive financial information.

Mobile Banking Experience

The Qonto mobile app enables business owners to manage finances from anywhere.

App features include:

- Instant payment notifications

- Transfer initiation

- Receipt uploads

- Expense tracking

- Card management

- Team oversight

This flexibility makes the Smart plan particularly appealing to entrepreneurs who work remotely or travel frequently.

Advantages and Potential Limitations

Advantages

- Easy online account setup

- Transparent pricing

- Strong expense management tools

- Useful accounting integrations

- Professional business banking features

- User-friendly interface

Potential Limitations

- Monthly fees may exceed basic plans

- Some advanced features require higher-tier subscriptions

- Availability depends on supported countries

Businesses should compare available plans to determine the best fit for their operational requirements.

Who Should Consider the Qonto Smart Plan?

The Qonto Smart Business Account Plan is a strong choice for freelancers, startups, and small businesses seeking a digital banking solution that combines business banking, expense management, and accounting automation in one platform.

With features such as higher transaction limits, integrated bookkeeping tools, team access controls, and real-time financial visibility, the Smart plan helps business owners save time and maintain better control over their finances.

For businesses moving beyond basic banking needs, the Qonto Smart plan offers a practical balance between cost and functionality.

Start your Qonto Smart application today and transform how you manage your freelance business.